Did you know that bank credit cards charge a whopping 4.8X more in interest than the bank pays you to borrow the same money? This may be a great setup for these banks, but not for average Americans. Fortunately, fintech offers a better way out.

The latest figures released by the Federal Reserve shows Americans’ credit card balances now exceed an unprecedented $1 trillion, a 43% increase since April 2021. Even more alarming is that delinquency rates on those credit cards have more than doubled during this same period.

With almost 40% of American adults now struggling to make ends meet each month, the consumer debt crisis is only going to intensify.

To make matters worse, as individual credit card balances reach record highs, household savings are falling to their lowest levels since 2009.

With data like this, is it any wonder that nearly 77% of Americans are losing sleep over money worries?

Fortunately, fintech (financial technology) is here to help alleviate today’s rash of “financesomnia.”

As illustrated below, using the government’s averages, fintech products offer more practical ways for Americans to amass money and pay down their debt.

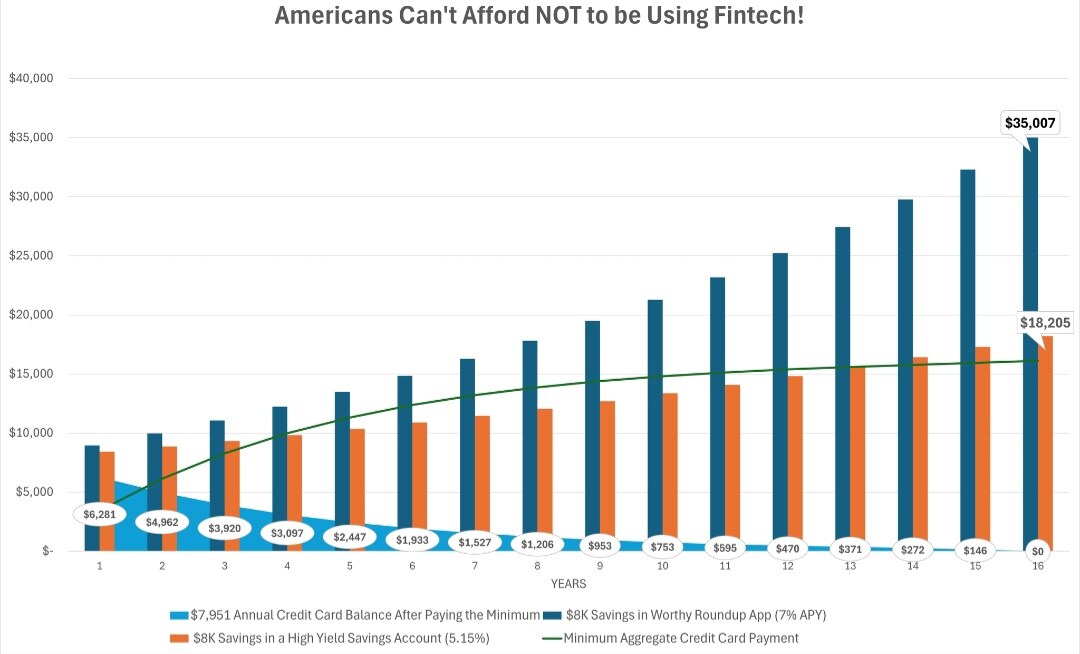

Based on data from the Federal Reserve and the U.S. Census Bureau, the average credit card debt in America is $7,951 - almost equivalent to the $8,000 median savings account, according to the Federal Reserve's most recent Survey of Consumer Finances.

The average credit card interest rate in America today is 24.66% — the highest since LendingTree began tracking rates monthly in 2019. On the other hand, the best high-yield savings account rate from a nationally available institution is currently only around 5.15%. While these conditions allow banks to effortlessly net 4.8 times more on its core product (you), the vast majority of individuals continue to suffer financially.

It is impossible for individuals to pay off this debt in a timely fashion - let alone save any money at all - when they are lending at 5.15% (at best) and borrowing at 24.66%.

In fact, it would cost over $16,000 and take over 16 years for an individual to pay off today’s $7,951 credit card balance by shelling out the minimum amount due each month. Keeping one’s $8,000 in today’s highest yield savings account would only be worth a little over $18,000 over that same 16-year period.

Spending $16,000 to pay off a $7,951 credit card balance while simultaneously accumulating only $18,000 in a savings account is not financially prudent. After accounting for taxes and inflation, anyone employing this strategy would end up with annual losses well into the double digits.